Mezinárodní rámec profesní praxe interního auditu

Nová podoba Mezinárodního rámce profesní praxe interního auditu byla oficiálně oznámena 6. července 2015 na Mezinárodní konferenci Mezinárodního institutu interních auditorů ve Vancouveru.

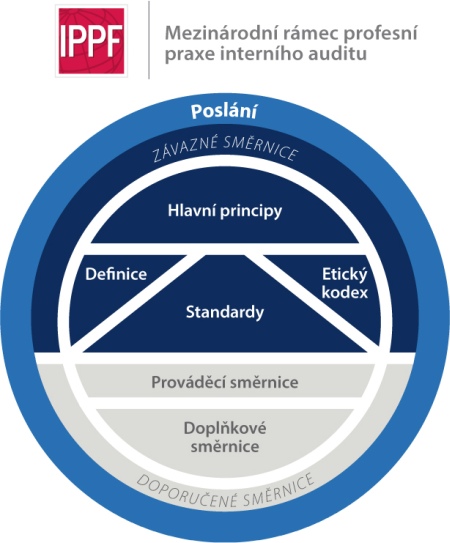

Poslání interního auditu vyjadřuje cíle, o jejichž dosažení interní audit pro danou organizaci usiluje. Zahrnutí Poslání do nového IPPF je záměrné a ukazuje, jak využít celý rámec k tomu, aby odborníci dokázali Poslání naplnit.

Hlavní principy, jako celek, vyjadřují účinnost interního auditu. Aby bylo možné útvar interního auditu považovat za účinný, měly by být účinným způsobem zavedeny všechny Principy. Způsob, kterým interní auditor, podobně jako útvar interního auditu, prokazuje splnění Hlavních principů, se může podstatně lišit mezi jednotlivými organizacemi. Nicméně neschopnost dosažení jakéhokoli z Hlavních principů by mohla vést k závěru, že útvar interního auditu nebyl tak účinný, jak by při naplňování Poslání interního auditu mohl být.

Copyright © The Institute of Internal Auditors

Copyright © Český institut interních auditorů

K získání povolení k překladu, změnám nebo reprodukci jakékoli části amerického originálu nebo českého překladu kontaktujte:

Český institut interních auditorů, z.s.

Karlovo náměstí 3, 120 00 Praha 2

Tel.: 224 919 361

The Mission of Internal Audit articulates what internal audit aspires to accomplish within an organization. Its place in the New IPPF is deliberate, demonstrating how practitioners should leverage the entire framework to facilitate their ability to achieve the Mission.

The Core Principles, taken as a whole, articulate internal audit effectiveness. For an internal audit function to be considered effective, all Principles should be present and operating effectively. How an internal auditor, as well as an internal audit activity, demonstrates achievement of the Core Principles may be quite different from organization to organization, but failure to achieve any of the Principles would imply that an internal audit activity was not as effective as it could be in achieving internal audit’s mission.

- Definition of Internal Auditing

- Code of Ethics

- International Standards for Professional Practice of Internal Auditing

Copyright © The Institute of Internal Auditors

Copyright © Český institut interních auditorů

K získání povolení k překladu, změnám nebo reprodukci jakékoli části amerického originálu nebo českého překladu kontaktujte:

Český institut interních auditorů, z.s.

Karlovo náměstí 3, 120 00 Praha 2

Tel.: 224 919 361

Doporučené směrnice jsou dostupné pouze pro členy ČIIA po přihlášení do členské sekce.

Copyright © The Institute of Internal Auditors

Copyright © Český institut interních auditorů

K získání povolení k překladu, změnám nebo reprodukci jakékoli části amerického originálu nebo českého překladu kontaktujte:

Český institut interních auditorů, z.s.

Karlovo náměstí 3, 120 00 Praha 2

Tel.: 224 919 361

Recommended Guidance are available only for members of IIA Czech after signing-in to the members‘ section.

Copyright © The Institute of Internal Auditors

Copyright © Český institut interních auditorů

K získání povolení k překladu, změnám nebo reprodukci jakékoli části amerického originálu nebo českého překladu kontaktujte:

Český institut interních auditorů, z.s.

Karlovo náměstí 3, 120 00 Praha 2

Tel.: 224 919 361